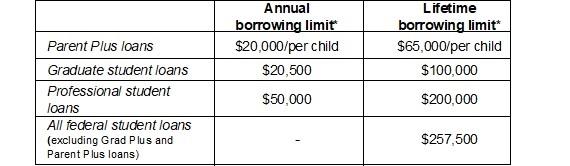

· Elimination of Grad PLUS loans. Starting July 1, 2026, Grad PLUS loans, which allowed graduate students to borrow up to the full cost of attendance, will no longer be available to new borrowers. · Legacy provisions. If an undergraduate or graduate student or a parent borrowed through a Federal Direct Loan program before July 1, 2026, they can continue to borrow from the program under current loan limits for three academic years or until they receive a credential, whichever is less, according to the National Association of Student Federal Aid and Administration (NASFAA). Here are the basics of the revised repayment options: · Repayment plans for new borrowers. For federal student loans made after July 1, 2026, the only repayment options available will be: 1) a new standard repayment plan, or 2) a new income-based repayment (IBR) plan called the Repayment Assistance Plan (RAP). The new program, RAP, requires borrowers to make loan payments of one to 10 percent of their income, with a minimum payment of $10. The repayment period is 30 years. · Repayment plans for current borrowers. Anyone who is enrolled in one of the following repayment plans – the Income-Contingent Repayment (ICR), Pay as You Earn (PAYE) or Saving on a Valuable Education (SAVE) plans – can remain in that plan until July 1, 2028. However, they must transition into a different plan – either the current IBR, the current standard plan, or RAP – by that date. If they do not, they will automatically be moved to RAP. The current IBR plan was changed so borrowers do not need to demonstrate partial financial hardship. In addition, balances of loans repaid may be cancelled after 25 years for current borrowers or 20 years for new borrowers. Consolidation loans used to pay off Parent PLUS loans must begin repayment before July 1, 2026, to qualify for IBR. As a result, parent borrowers who prefer to have an income-based option for loan repayment should consider consolidating their loans before that date, according to Student Loan Borrower Assistance at the National Consumer Law Center. · All loans must be repaid from the same repayment plan. · Higher K-12 withdrawal limits for 529 plans. In addition to expanding the “qualifying” education expenses, OBBBA increased the amount that may be withdrawn for qualified primary and secondary school expenses from $10,000 to $20,000. If you have questions or would like to discuss your college funding plans, please get in touch. WEEKLY FOCUS – THINK ABOUT IT “Knowledge is power.” ― Sir Francis Bacon, Philosopher |